Markets don’t usually announce turning points. They move quietly, drift for long stretches, and only look obvious in hindsight. The New Zealand housing market in late 2025 is a good example of that kind of subtle shift – the kind that feels uneventful day to day, but meaningful when you zoom out.

Back in September, we noted a market beginning to steady. A month on, that pattern is clearer.

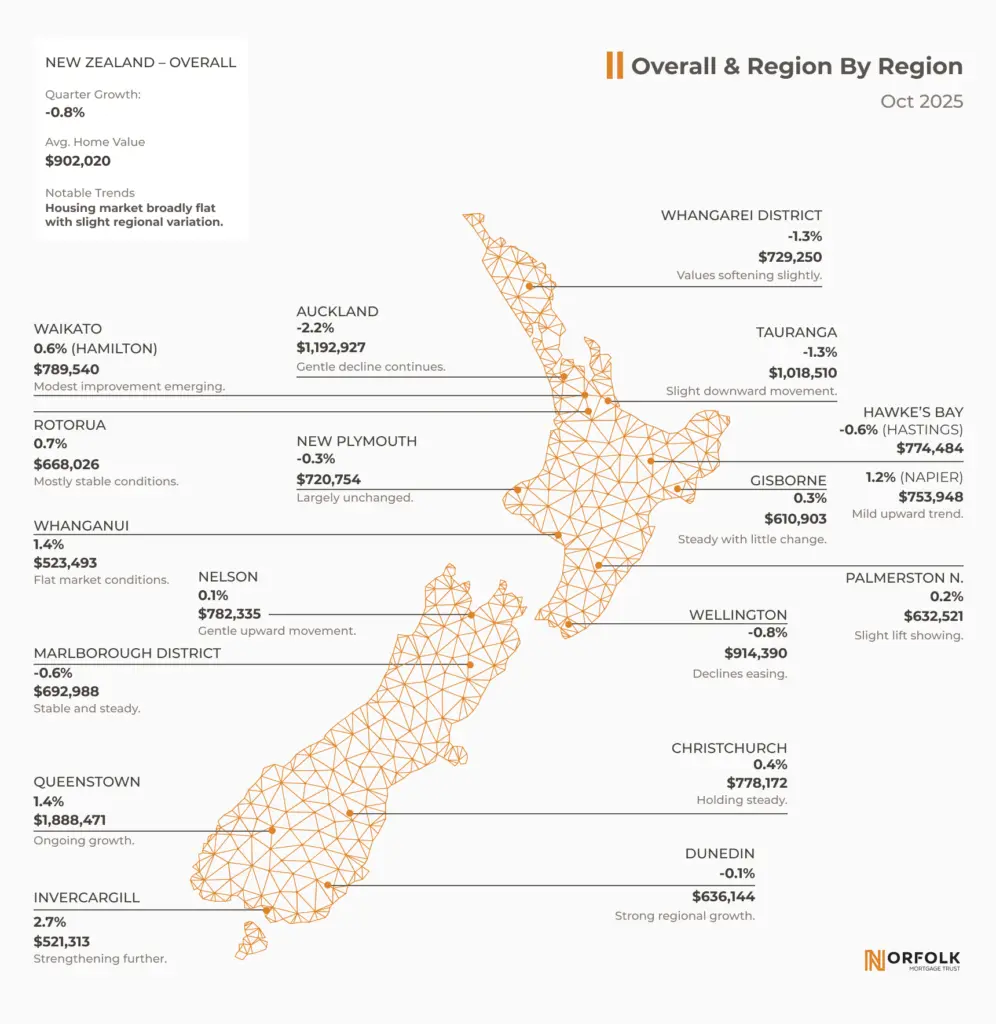

The latest QV data shows national home values are now down just 0.8% over the quarter, sitting at $902,020 – almost exactly where they were a year ago. Prices are still well below their early-2022 peak, but the pace of decline has slowed. And in several regions, particularly in the South Island, the numbers have begun to tick upward.

Markets often reveal their character when they stop moving fast. When the dust settles, you can see what’s real.

What the Latest Numbers Show

The market isn’t booming. It isn’t collapsing. It’s doing something more interesting: it’s finding balance.

Still soft:

- Auckland: –2.2%

- Wellington City: –0.8%

- Tauranga: –1.3%

- Whangārei: –1.3%

These areas are still digesting the economic pressure of the last couple of years.

Holding steady:

- Christchurch: +0.4%

- Hamilton: +0.6%

- Nelson: +0.1%

- Palmerston North: +0.2%

These are markets where equilibrium is quietly returning.

Gaining ground:

- Invercargill: +2.7%

- Queenstown: +1.4%

- Napier: +1.2%

- Dunedin–Taieri: +6.9%

- West Coast districts: Westland +3.4%, Buller +2.8%, Grey +0.4%

Early signs often show up in smaller markets before they flow into the big centres.

That’s what’s happening here.

Buyer activity has picked up with spring, lending constraints have eased, and confidence is improving – but unevenly. That unevenness isn’t a bug. It’s how most recoveries actually work.

Why Stability Matters More Than Headlines

Headlines love drama, but long-term investors usually don’t benefit from it.

When people ask whether a market has “hit the bottom,” what they’re really asking is whether fear or optimism is about to take control. But for income-focused investors – the kind who care more about reliability than adrenaline – the better question is: What conditions reward discipline?

Right now, three forces are working in the property market:

1. Fundamentals take centre stage again.

When prices surge, almost everything looks like a good idea. When they flatten, quality stands out. Conservative loan-to-value ratios, strong borrowers, and sound underwriting matter more in a steady market, because there’s less noise covering up bad decisions.

2. Lower volatility is good for lenders.

Mortgage investments don’t rely on speculation; they rely on structured repayments. When prices aren’t swinging wildly, those repayments become more predictable – assuming lending remains disciplined.

3. Regional strength supports overall security.

Outperformance in places like Dunedin–Taieri, Invercargill, and Queenstown bolsters the underlying property base for nationwide lenders. When resilience is spread widely, risk spreads out too.

Stability may not feel exciting, but we see it as an underrated superpower.

What This Means for Norfolk Mortgage Trust Investors

Over nearly 20 years, Norfolk Mortgage Trust has seen markets rise, fall, overheat, cool, and everything in between. The lesson across all those cycles is surprisingly consistent: principles outperform predictions.

Norfolk’s conservative approach – low loan-to-value ratios, careful borrower selection and property-backed lending – is built for markets exactly like this.

That discipline has allowed Norfolk to deliver uninterrupted monthly returns since 2006 – including during far more volatile periods than the one we’re in now.

Current Snapshot (October 2025)

- Annualised pre-tax return: 6.5% p.a.

- Funds under management: $53m+

- Investor activity: $1.8m invested in October

Consistency doesn’t make headlines. But it does build trust.

Where the Market May Go Next

The most likely outcome for the year ahead is a steady finish to 2025, followed by gradual growth through 2026 as:

- interest rates ease

- employment strengthens

- household confidence returns

- seasonal activity picks up

Growth will vary by region. Big cities may take longer to gather momentum, while South Island and selected regional markets continue to lead.

But the lesson here is an old one: trying to time the exact bottom is less productive than sticking to a sound process. The aim isn’t to predict the turning point – it’s to stay positioned sensibly before, during, and after it.

In Times of Change, Consistency Becomes a Strength

WEven as the market stabilises, uncertainty always lingers at the edges. The goal isn’t to eliminate it – that’s impossible. The goal is to invest in a way that remains rational through every phase of the cycle.

Norfolk Mortgage Trust is built on that idea: stable, property-backed income; careful lending; and a long history of guiding investors through changing conditions.

If you value discipline over prediction, and stability over speculation, Norfolk is ready to support your next step.

Learn more at norfolktrust.co.nz

Invest with Confidence. Invest with Norfolk Mortgage Trust.

Data Source: QV House Price Index, October 2025