Markets rarely pivot dramatically. More often, they recalibrate quietly – shifting from decline to consolidation, from uncertainty to cautious confidence.

The New Zealand property market at the start of 2026 appears to be in exactly that phase.

Back in October, we noted early signs of the market finding its footing. The January 2026 QV House Price Index now confirms that transition more clearly. The broad-based declines that defined much of the past 2 years have largely run their course.

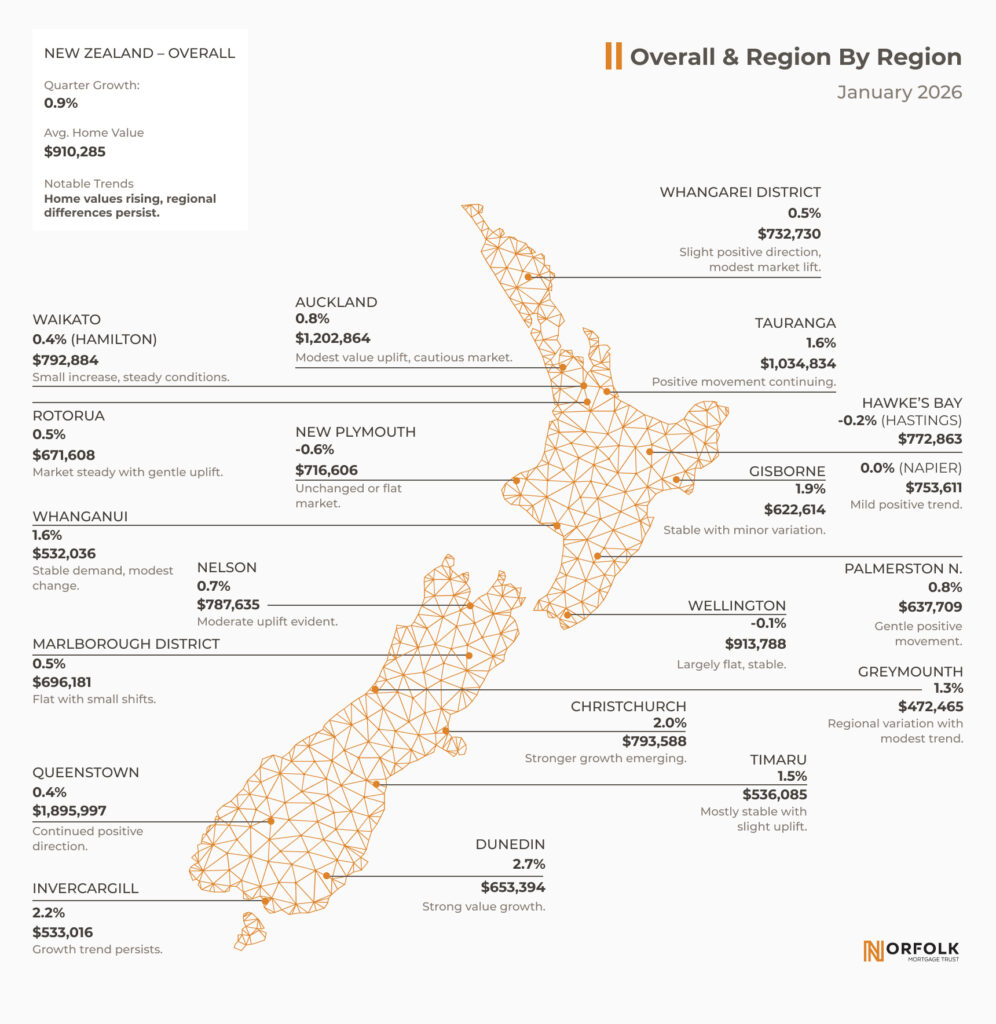

Nationwide residential property values rose 0.9% over the 3 months to January, with the average home now sitting at $910,285, which is:

- 0.4% higher than this time last year

- 13.1% below the January 2022 market peak

Not booming. Not falling. Rebalancing.

For income-focused investors, this kind of environment is often preferable to rapid swings. Stability creates room for disciplined lending and structured returns.

A Market Shaped by Local Fundamentals

If there’s one clear takeaway from the January QV report, it’s this:

There is no single nationwide surge – and no broad-based decline.

Instead, local conditions are driving outcomes. Employment trends, housing supply, regional industries and affordability are shaping performance market by market.

Lower interest rates have improved borrowing capacity for some households. But buyers remain measured. There is no urgency. No speculative rush. No widespread retreat.

That absence of extremes matters.

When momentum no longer dominates, fundamentals reassert themselves. And that’s typically when disciplined lending matters most.

Where Values Are Moving

Leading quarterly growth:

- Dunedin: +2.7%

- Christchurch City: +2.0%

- Tauranga: +1.6%

Christchurch continues to demonstrate resilient demand, supported by a strong construction pipeline across Christchurch, Selwyn and Waimakariri. Dunedin’s performance reinforces a pattern seen in prior cycles – regional strength often emerges before major metropolitan centres regain momentum.

These increases are measured, not speculative. They reflect underlying demand rather than exuberance.

Modest upward movement:

- Auckland Region: +0.8%

- Hamilton: +0.4%

Despite elevated stock levels, Auckland prices have remained steady overall, with selective uplift in parts of Auckland City and the North Shore. First-home buyers remain active, while developers gradually bring new supply to market.

This is consolidation, not acceleration.

Effectively flat:

- Wellington City: –0.1%

Wellington remains subdued. High listing volumes and softer employment conditions are containing price pressure. Buyers have options – and bargaining power.

Taken together, the national picture is one of moderation.

For investors, moderation reduces unpredictability. And predictability reduces regret.

What This Means for Income-Focused Investors

For investors seeking reliable returns rather than short-term speculation, this phase of the property cycle matters.

Three shifts are particularly important:

1. The Downward Momentum Has Eased

The sharp correction phase appears to have stabilised. While values remain below peak levels, broad-based declines are no longer the defining feature of the market.

For lenders, this reduces downside velocity risk.

2. Lower Volatility Supports Conservative Lending

When prices move gradually rather than sharply, lending decisions can focus on serviceability, borrower quality and conservative loan-to-value ratios – not market timing.

Predictable markets favour structured processes.

3. Regional diversity spreads risk

With different regions performing differently, risk is not concentrated in a single overheated centre. A diversified, property-backed lending approach benefits from this spread of underlying security.

Stability may not make headlines. But for income-focused investors, it often creates the most durable conditions.

When Markets Rebalance Fundamentals Become Important Again

Norfolk Mortgage Trust has operated through multiple property cycles over nearly two decades – periods of rapid growth, sharp contraction, and consolidation like the one unfolding now.

Across every phase, one principle has remained constant:

Disciplined lending.

Norfolk’s approach is structured around:

- Conservative loan-to-value ratios

- Careful borrower assessment

- First mortgage security over residential property

- Active monitoring of regional market conditions

Operating across multiple regions also reduces concentration risk. When different parts of the country move at different speeds, diversification strengthens overall portfolio resilience.

In a market defined by consolidation rather than exuberance, that discipline becomes a genuine competitive advantage. It is the same disciplined approach that has enabled Norfolk to deliver uninterrupted monthly returns since 2006 – including through periods far more volatile than today’s.

Current Snapshot (January 2026)

- Annualised pre-tax return: 6.5% p.a.

- Funds under management: $58m+

Consistency rarely makes headlines. But it builds trust over time.

Investing With Clarity In 2026

QV’s outlook suggests we are unlikely to see a rapid upswing in 2026. Instead, property values are expected to remain broadly steady, with pockets of modest movement shaped by familiar fundamentals:

- Interest rate movements

- Employment trends

- Household confidence

- Regional economic drivers

In short, 2026 is shaping up to be a year of gradualism rather than exuberance.

For property-backed lenders and income-focused investors, that kind of clarity matters more than excitement. Markets do not need dramatic surges to deliver reliable outcomes – they need rational conditions where fundamentals guide performance.

Norfolk Mortgage Trust is built around those fundamentals:

property-backed lending, conservative structures and consistent income generation.

For investors seeking stability in an uneven economic environment, that approach is not just reassuring – it’s strategic.

Learn more at norfolktrust.co.nz

Consistent income. Property-backed. Disciplined – Norfolk Mortgage Trust.

Data source: QV House Price Index, January 2026.