The latest QV House Price Index isn’t grabbing headlines – but it should have investors paying attention.

New Zealand’s property market has moved beyond correction. Prices are holding. Volatility has eased. And while that may lack the drama of boom or bust, it represents something far more valuable: clarity.

For income-focused investors, this is the kind of market environment that matters most.

A Market Holding Steady

When price volatility fades, the drivers of return shift. Outcomes rely less on timing and more on how investments are structured.

In a market that no longer rewards timing, the advantage shifts to those built for consistency.

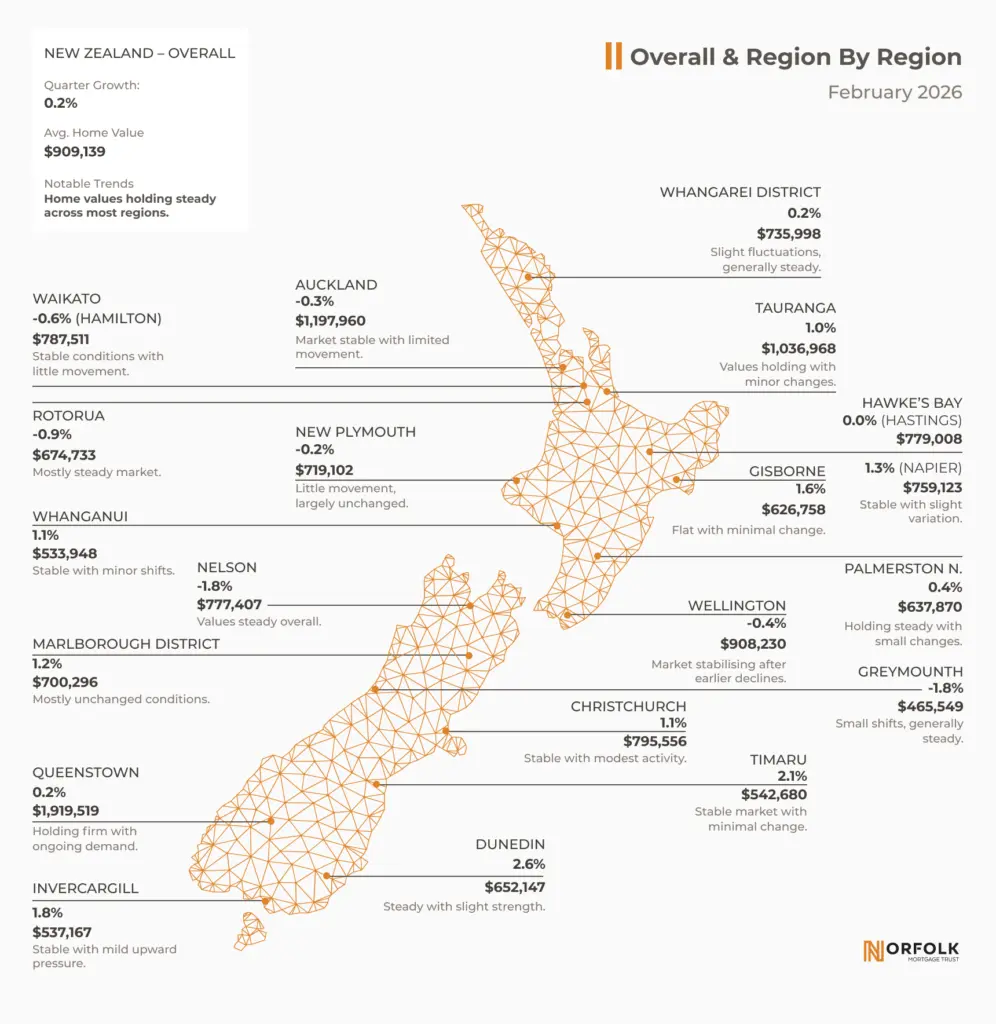

According to QV’s February data, the average residential home value rose just 0.2% over the quarter, bringing the national average to $909,139. Values are still 0.4% below this time last year – but remain 21.5% higher than March 2020.

QV spokesperson Simon Petersen described it as one of the flattest summers for home value growth in recent memory, noting that activity has remained surprisingly resilient.

“Residential property values have remained largely static this quarter, and yet the housing market has continued to tick along with activity remaining relatively robust in many parts of the country,” he said.

“Steady as she goes” is an accurate summary – but for investors, the more important question is what that stability changes.

A Market Driven by Local Conditions

Beneath the national averages, a clearer trend is emerging: the New Zealand property market is becoming increasingly fragmented.

Stronger momentum is concentrated in parts of the South Island, where demand remains resilient and supply pressures are more contained:

- Dunedin: +2.6%

- Timaru: +2.1%

- Invercargill: +1.8%

- Christchurch: +1.1%

Meanwhile, larger North Island centres are still adjusting:

- Auckland: –0.3%

- Wellington: –0.4%

- Waikato: –0.6%

This isn’t just variation – it’s fragmentation. The idea of a single “New Zealand property market” is becoming less useful.

For investors, outcomes are now increasingly determined by where and how capital is deployed – reinforcing the importance of diversification and disciplined asset selection.

What Stability Actually Changes

Flat markets are easy to overlook. Without rapid growth or sharp declines, there’s less urgency – and fewer headlines.

But for income-focused investors, these conditions often provide the clearest environment for decision-making.

When prices move sideways:

- Returns become less dependent on market direction

- Risk becomes more visible

- Structure becomes the primary driver of outcomes

Stability doesn’t remove risk – it reveals who has been managing it properly.

Discipline as the Actual Advantage

Every phase of the property cycle rewards different behaviours.

- Growth markets reward momentum

- Downturns expose weak structures

- Stable markets favour discipline

Right now, we’re firmly in that third phase.

Without price growth to mask risk, outcomes are tied directly to fundamentals: serviceability, security, and underwriting discipline.

For example, in a flat market, a marginal loan with stretched serviceability is quickly exposed. A conservatively structured loan, by contrast, continues to perform as intended – regardless of market movement.

For investors, consistency isn’t achieved through timing. It’s achieved through repeatable, well-managed processes applied across every phase of the cycle.

How Norfolk Is Positioned in This Environment

Norfolk Mortgage Trust is structured for exactly this kind of market.

Every loan is built on first mortgage security, conservative loan-to-value ratios, and careful borrower assessment. These aren’t settings that adjust with the market – they’re the constants that have defined every lending decision since inception.

Operating across multiple regions adds another layer of resilience, particularly as market performance becomes more localised.

But the most compelling measure isn’t the framework itself – it’s what that framework has delivered.

Since 2006, Norfolk has provided uninterrupted monthly investor returns – across the GFC, COVID disruption, and multiple property cycles. Through all of it, the approach hasn’t changed. Neither has the focus on protecting investor capital while delivering consistent income.

As at February 2026:

- Annualised pre-tax return: 6.5% p.a.

- Funds under management: $58m+

Performance built on discipline is often less visible in the short term – and considerably more reliable over time.

Investing with Clarity in 2026

QV’s latest commentary suggests the market is likely to remain relatively steady in the near term, with movement driven by familiar factors: interest rates, economic conditions, and regional dynamics.

For investors, that reduces the need to predict what happens next.

Instead, it sharpens the focus on what can be controlled: structure, discipline, and risk management.

In a market that no longer rewards timing, consistency becomes the advantage.

That’s where Norfolk is positioned.

Learn more at norfolktrust.co.nz

Explore how Norfolk delivers consistent, property-backed income at norfolktrust.co.nz

Data Source:QV House Price Index, February 2026