Last month, we noted that New Zealand’s property market had found its footing.

The latest QV House Price Index suggests something more definitive: that footing is holding – and beginning to look like the new normal.

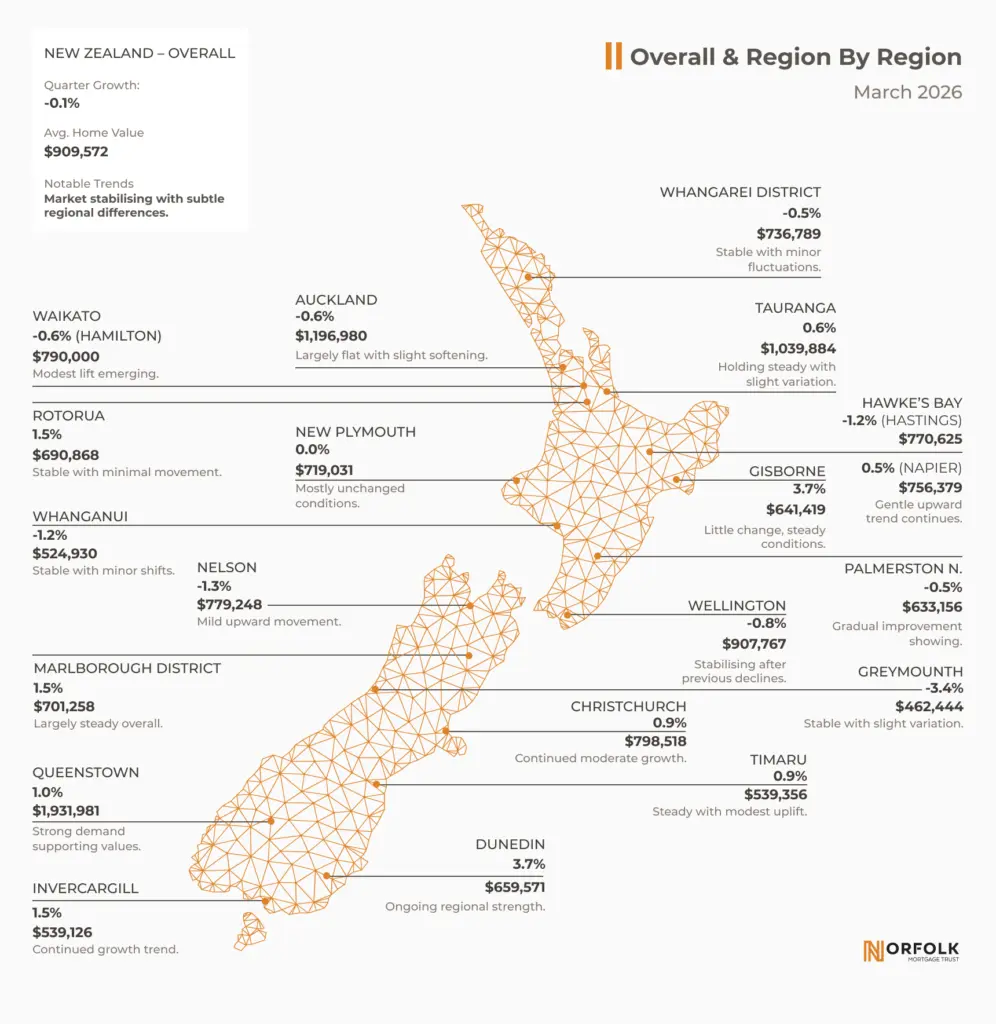

National home values are now sitting 21.6% higher than they were in March 2020, but growth has slowed to a near standstill, with values easing just 0.4% over the past year and 0.1% over the most recent quarter.

These aren’t headline-grabbing numbers. But for investors, they signal something more important than growth: stability that’s proving durable.

A Market That’s No Longer Searching for Direction

Through 2024 and 2025, the key question was whether the market had truly stabilised – or was it simply pausing between cycles.

That uncertainty is starting to fade.

The latest QV data shows:

- Price movements are consistently modest

- Activity levels are tracking closer to long-term averages

- Buyers and sellers are behaving more like they used to

In practical terms, urgency has left the market. Buyers are taking their time. Vendors are meeting the market. Negotiation has returned.

This is no longer a market driven by momentum. It’s one shaped by the basics – affordability, interest rates and supply.

And that shift matters.

Because when markets behave more predictably, the risk of sharp corrections reduces – and investment decisions become less about timing, and more about structure.

A Fragmented Market, Not a Uniform One

As stability has taken hold, another trend has become clearer: performance is increasingly local.

Some regions are continuing to show resilience:

- Christchurch and wider Canterbury remain steady, with ongoing modest growth

- Otago has outperformed nationally in early 2026, with stronger quarterly gains and lifestyle demand

Others are still adjusting:

- Auckland values are down 3.8% year-on-year

- Wellington has seen a 5% annual decline

- Parts of the North Island remain flat or slightly negative

This divergence reinforces an important point: there is no single “New Zealand property market” anymore. Outcomes are increasingly shaped by local supply, demand and economic conditions.

For investors, that raises the bar. It’s no longer enough to be in the market – you need to be positioned correctly within it.

What a Predictable Market Changes

Flat markets often go overlooked. Without rapid growth or sharp declines, there’s less noise – and less urgency.

But this is the environment where investment structure matters most.

When prices aren’t doing the work, returns depend on how an investment is put together: what it’s secured against, how risk is managed, and how income is generated.

In other words, the market stops carrying performance – and the design of the investment starts to.

Why Income Is Back in Focus

With capital gains less certain, the focus for many investors is shifting – back toward income and consistency.

That’s particularly relevant in today’s environment:

- Interest rates remain a consideration

- Cost-of-living pressures are still present

- Investor activity in direct property remains subdued

At the same time, property as an asset class continues to demonstrate resilience. Even after recent adjustments, values remain materially higher than pre-2020 levels.

The opportunity, then, isn’t necessarily in chasing growth – it’s in accessing property-backed returns in a more controlled way.

Where Norfolk Mortgage Trust Fits

Norfolk Mortgage Trust is structured for exactly this kind of market.

Rather than relying on property price growth, returns are generated through secured lending, backed by real property assets.

That distinction becomes more valuable as markets stabilise.

Investors are increasingly looking for:

- Regular, predictable income

- Diversification across multiple loans and regions

- Reduced exposure to price volatility

- A hands-off approach to property investing

Norfolk delivers on those priorities.

As at March 2026, investors are receiving a pretax, annualised return of 6.5%, paid monthly – providing a consistent income stream regardless of short-term market movements.

The underlying approach remains unchanged:

- First mortgage security

- Conservative loan-to-value ratios

- Disciplined lending practices

In a market where outcomes are no longer driven by rapid growth, that consistency becomes the advantage.

Investing With Greater Clarity

The latest QV data doesn’t point to a market about to surge – or fall.

Instead, it points to something more sustainable: a property market that is balanced, predictable, and increasingly shaped by supply, demand and affordability.

For investors, that reduces the need to forecast what happens next.

And increases the importance of how investments are structured today.

In this environment, consistency isn’t just desirable – it’s where performance comes from.

Learn More

If you’re looking for a way to generate regular monthly income from property-backed investments – without the complexity of direct ownership – Norfolk Mortgage Trust offers a disciplined, proven approach.

To find out more, visit norfolktrust.co.nz or get in touch with our team.

Explore how Norfolk delivers consistent, property-backed income at norfolktrust.co.nz

Data Source:QV House Price Index, March 2026